The future of beauty-from-within does not lie in new ingredients. It is in the format that delivers them. While Western brands remain locked into dry formats due to outdated infrastructure, Asia has already proven that liquid nutricosmetics, daily collagen drinks and beauty shots, drive higher retention, premium pricing, and stronger margins. This shift is creating a structural transformation, creating an emerging oligopoly for those who master liquid formulation, flavor masking, and shelf-stable delivery. With consumer demand rising fast in North America and Europe, and over €3.7 billion in ex-factory turnover at stake, the brands and manufacturers that scale liquid correctly will own the next generation of wellness rituals. TOSLA was built to serve this shift not with product, but with the infrastructure behind the ritual.

Beauty from within is evolving and taking new forms. The next $50 billion opportunity in supplements isn’t about new pills or rebranded powders. It’s about something more tangible: daily liquid rituals that people actually finish. In many parts of Asia, this is already common. Beauty drinks sit alongside cold brews in Tokyo and convenience stores in Seoul, priced at a premium and bought repeatedly. The formula needs the right ingredients and, most importantly, the right format. Taste influences habits. Habits lead to repeat purchases.

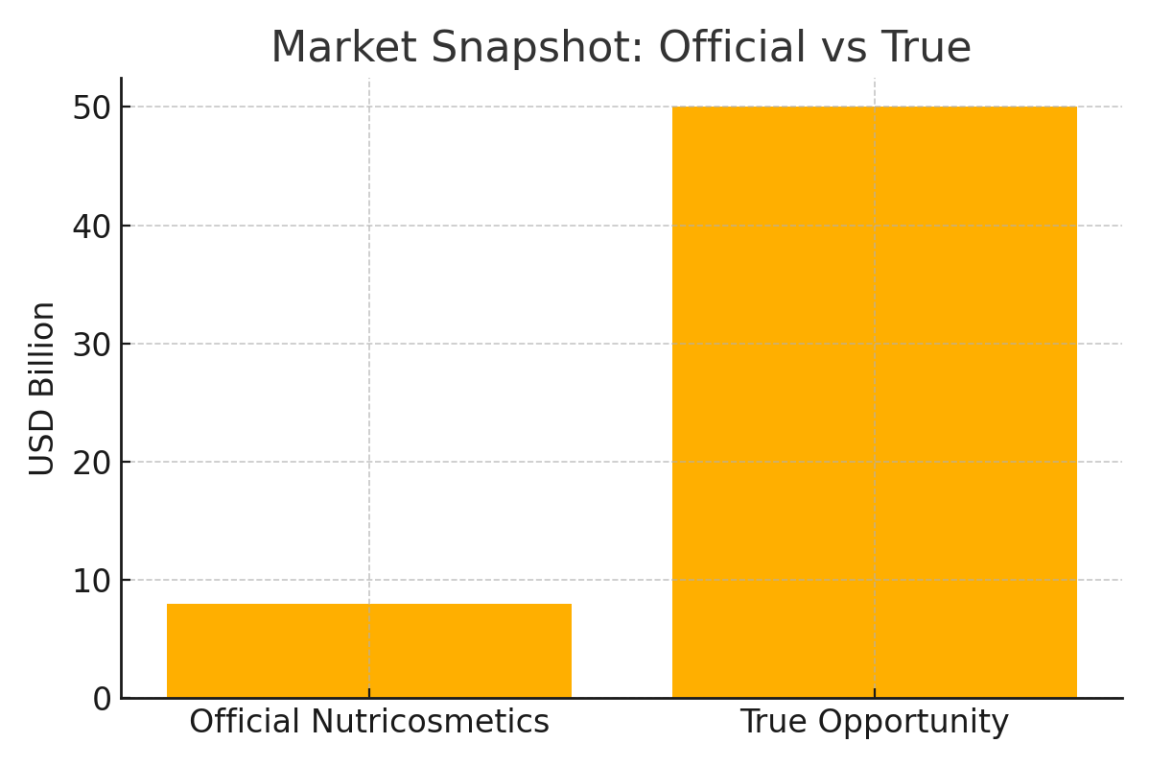

In the West, demand is catching up, but infrastructure isn’t. While consumers are increasingly willing, most brands remain limited to capsules, sachets, and gummies that rarely last beyond the third purchase cycle. Official valuations peg the beauty supplement market at $8 billion [1], a modest figure compared to the larger VMS sector. But if you follow where spending actually occurs, across collagen shots, functional elixirs, and drinkable blends, the number approaches $50 billion. The key? A format that fosters daily rituals.

What makes liquids unique is their ability to be absorbed, their flavor, and their capacity to anchor routines. In a market driven by loyalty, routine becomes everything. Unlike dry supplements that are shelved and forgotten, liquids stay in the fridge, on the counter, or beside the toothbrush. They encourage engagement and thus become habitual.

That delivery, repeated and consistent, becomes the moat. A liquid ritual that’s enjoyable, effective, and reliable isn’t just a product; it’s a complete system. Once consumers integrate it into their daily routine, the stakes for quality and consistency increase. In this context, CDMO no longer simply means “contract manufacturer.” It now stands for “critical delivery.” Batch by batch, bottle by bottle, trust is earned, and it’s also difficult to regain once broken.

We’ve seen similar consolidation before. Energy drinks were once a chaotic, crowded shelf until Red Bull standardized the ritual. Now, beauty-from-within is going through its own alignment. The category is consolidating, and formats are aligning. A quiet oligopoly is emerging around those who can operationalize liquid ritual at scale.

The pressure is mounting on established beauty brands. If they delay, retailers will step in to fill the space, just like they did in the food sector. Private label wellness products are already growing over 11% year-over-year. Supermarkets and pharmacy chains are not focusing on launching more dry capsules. Instead, they are emphasizing relevance, and nutricosmetics are at the intersection of beauty, health, and everyday habits.

This shift goes beyond ingestibles, focusing more on the intersection of format, science, and consumer lifestyle, and on which players can turn that convergence into a sustainable habit. Skincare alone can no longer bear the burden. The new frontier is internal, and the winners will master taste, science, and frequency with one captivating, liquid action.

We believe the winners in this space will be those who build integrated systems of formulation, flavor, and delivery, rather than those chasing short-term hype.

For years, contract manufacturing in wellness was a commodity business with interchangeable lines producing pills and powders with few barriers to entry. But liquids changed that dynamic. Flavor science, shelf-life preservation, and consumer palatability introduced new complexities. The manufacturers who mastered these layers now hold the keys to a rapidly closing club. Their value extends beyond production into the cultural sphere. They help brands move beyond simple formulas into rituals, and rituals are where long-term margins thrive.

This is why scale alone is no longer enough. To compete in this emerging oligopoly, a brand must embed itself into an ecosystem that combines formulation agility with sensory intelligence, where taste serves as a strategic moat. Since these ecosystems are limited and the technology behind them is costly to replicate, access becomes the new currency. The next five years won’t be defined by how many SKUs you launch, but by who bottles them and whether they can do so flawlessly, month after month.

The Untapped Beauty-From-Within Force

For all its shimmer and market momentum, the beauty industry, especially skincare, is struggling under the weight of its own promises. In the U.S., prestige skincare has reached a plateau. Circana’s latest data shows that while mass-market beauty continues to grow modestly, it is mostly driven by pricing rather than volume. In Europe, quarterly earnings calls tell a similar story: even industry giants like Estée Lauder and Coty recognize that their most loyal customers are hesitant. The reason? A more knowledgeable, skeptical consumer who reads ingredient lists, questions miracle claims, and knows when a jar of cream will not deliver what it promises.

Shelf space reflects the same tension. What was once a free-for-all of SKUs has become a pressure test. More options no longer indicate growth. Investors now expect brands to justify every launch, narrow their ranges, and focus on products that can withstand scrutiny. Flash alone doesn’t sell. Margins, science, and stickiness do. That’s why biotech serums, dermo cosmetics, and functional formats are attracting capital, while influencer-founded vanity lines are losing momentum.

The old game was about shelf presence. The new game is about defensibility. And defensibility doesn’t come from a TikTok trend but from formats and systems that deliver consistent value. Brands that cross the mirror from the skin to the gut and back are the ones gaining ground. Nutricosmetics, long considered a fringe category, are proving to be the natural progression for consumers tired of hype and hungry for results that can’t be rinsed off. When margins are squeezed by discounting and dupe culture, rituals and not one-off purchases become the foundation of loyalty.

That’s why players like Shiseido quietly dominate the beauty-from-within market in Asia. It’s why prescription-grade skincare and dermatologist-led brands are outpacing generic “clean beauty” lines. The next generation of acquisition targets won’t be found in bathroom cabinets. They’ll be in fridges, gym bags, carry-ons—wherever consistent routines are built. The strongest brands are shifting focus from just topicals. They’re combining ingestion, application, and data to build barriers that a one-time shelf presence never could.

This cultural shift aligns with the financial one. Gen Z isn’t browsing beauty counters like their predecessors did. They’re reading INCI lists on TikTok, watching before-and-after videos, and demanding evidence instead of just adjectives. They understand that stress, diet, and hormonal changes impact skin more than any serum ever could. They want solutions that move with them and aren’t just sitting next to the bathroom sink. From personalized diagnostics to daily supplements, they’re shopping for regimens, not just routines.

This doesn’t mean skincare is outdated. It means it’s unfinished. The next wave of beauty innovation won’t discard topicals, but it will integrate them into a broader, smarter ecosystem. For founders, chemists, and brand leaders, the challenge is clear: move beyond packaging battles and focus on long-term consumer value. The easy profits driven by hype, celebrity, and Instagrammable jars are fading. What’s growing in their place is more difficult to earn: loyalty based on habit, trust, and science.

Because beauty has always reflected culture, and culture is changing. The idea of transformation remains compelling, but now consumers want to understand what’s underneath the surface. Why does it work? What happens when the water hits my face? What am I doing for my skin ten years from now, not just tonight?

And that “what else” already has a name: nutricosmetics. The idea that beauty begins below the surface has been around for decades in Asia, where collagen drinks and hyaluronic shots are as common as afternoon tea. But in the West, that concept stalled and was reduced to novelty powders, a few gummies, and a shelf that couldn’t deliver on the ritual.

The main idea isn’t complicated: beauty from within only works when it fits modern life. Taste, convenience, and routine matter more than hero claims or exotic extracts. Liquid formats meet that need. One sip becomes a habit. A habit forms a loop. That loop, where science meets experience, and ritual becomes repetitive, is where the future of the category lies.

Contrast this with the traditional VMS aisle: tubs of collagen that never get opened, pill bottles that gather dust, gummies that go stale before the jar is empty. These formats actively hinder habit formation. Ironically, because the actives themselves, from vitamins to peptides, are well-studied and effective. But it’s not what’s inside that fails. It’s how it’s delivered.

This is where compliance becomes the true product. Studies have shown that even dedicated supplement users stop after the second or third bottle. According to Glanbia Nutritionals, “pill fatigue” is a common problem, especially in multi-dose routines. About 40% of U.S. adults take supplements daily, but the dropout rate increases when more than two pills are needed. Gummies, once celebrated as a fun alternative, come with their own issues: low dosages, added sugars, and consumer boredom. Verywell Health notes that many users quit after a few bottles, citing lack of results and extra calories.

Liquid formats, by contrast, offer several advantages. They’re easier to swallow, faster to absorb, and crucially, easier to integrate into real life. No mixing. No measuring. No forgetting. And yet, Western shelves remain mostly empty. While Asia’s stores overflow with collagen drinks from Shiseido, ampoules from Fancl, and hyaluronic tonics from AmorePacific, the U.S. falls far behind. According to Grand View Research, liquid supplements accounted for only 13.4% of the American market in 2023 despite being the fastest-growing format worldwide. The issue isn’t demand or science; it’s supply.

Why? Because producing high-quality liquids at scale is difficult. It requires stable formulations, flavor engineering, and strict controls on light, oxygen, and microbial growth. Capsule factories can produce millions of tablets with little sensory complexity. Liquid production, on the other hand, is entirely different. In North America and Europe, only a few contract manufacturers have the capability, and even fewer are willing to take the risk. As a result, the status quo remains: familiar formats with familiar failures.

This resistance creates a self-fulfilling cycle. Brands assume liquids won’t scale, so they avoid investing in them. Retailers stock what’s safe. Supply chains remain optimized for powders and pills. Meanwhile, consumers wonder why the collagen they bought last spring still sits unopened behind the olive oil.

But the numbers are already changing. The global liquid supplement market is now worth $29 billion and is expected to grow past $45 billion by 2032. Gen Z and younger Millennials are leading this shift, opting for formats that suit their lifestyle: drinkable wellness shots, flavored sleep tonics, functional beauty waters. They don’t want another tub; they want something they’ll actually finish.

In short, the actives aren’t the problem. The format is. The VMS industry’s failure or refusal to scale liquid production remains one of its most significant blind spots. Science is solid. The demand is clear. Only the systems are lagging.

So here we are: the nutricosmetics market is still officially valued at $8 billion, while actual spending on beauty drinks, collagen shots, and functional elixirs quietly approaches $50 billion. This is not a prediction. It is a miscategorized reality, where a market exists in the margins, waiting for brands to recognize what consumers already do.

And the lesson from the factory floor is straightforward. Offer people a liquid product that works, tastes good, looks premium, fits into their lives, and they will return. They don’t forget. They don’t churn. They keep coming back. That’s not a marketing funnel. That’s a habit loop. And it’s already in motion.

In the pages ahead, I’ll show you what that cycle looks like in real consumer behavior because the future of beauty-from-within isn’t just a trend. It’s simply been overlooked, misfiled, and sitting plainly in sight all along.

The Miscounted Billions

Every major beauty forecast will tell you the same thing: nutricosmetics is an $8–10 billion niche tucked inside the larger VMS industry. Respectable, yes — but deceptive. Look beneath the surface, and you’ll see that these clean, separate categories don’t reflect how consumers actually shop.

When Western supplement aisles don’t offer dedicated beauty-from-within products, consumers get creative. They explore the joint health section, grab sports recovery powders, or purchase generic wellness capsules. Not because they’re training for a marathon, but because they understand MSM, glucosamine, collagen, and hyaluronic acid aren’t just for mobility — they’re also for skin, hair, and nails. The irony? A tub labeled “joint support” often ends up in the cart with a beauty goal in mind. These clear labels break apart the moment you look at the checkout data.

The numbers confirm this shift. In North America and Europe, collagen is still found mostly in the sports section or marketed for bone health. Globally, collagen supplements are traditionally linked to bone and joint health, which still makes up a large part of the market. However, conversations with sports nutrition brands show a clear change in consumer goals: more than two-thirds of their collagen buyers are actually looking for beauty benefits like firmer skin, better elasticity, and stronger hair. MSM and glucosamine tell the same tale. Marketed as mobility aids, peer-reviewed studies indicate they also improve skin structure and elasticity. Compared to many Western markets, there are almost no beauty-focused MSM or hyaluronic acid products, so consumers settle for the clinical-looking options, even if what they really want is a glow, not just movement.

This mismatch is as much about format as it is about claims. In Asia, collagen drinks and beauty shots have been staples for decades: simple, sensory, and easy to consume. In the West, the dominance of powders and oversized pills is a legacy of old manufacturing practices. Those formats are cheap to produce but poor for compliance. Retail data shows that collagen tubs and sports powders are purchased with enthusiasm and then abandoned, half-finished, under the sink. Gummies promised a fun alternative but underdeliver on dosage, added sugars, and lose their novelty quickly. The science is there; consumer interest is there. The problem lies in the delivery system.

Consumers today are informed and self-directed. They scroll Reddit threads, follow TikTok explainers, and decode ingredient lists like pros. They want multifunctional products and are willing to cross categories to get them. A joint health tub of hydrolyzed collagen becomes, in their minds, a beauty product. But this self-hack comes with a cost: bad flavor, gritty texture, and a format that feels medicinal rather than indulgent.

For brands, this disconnect reduces value. A sports collagen tub might sell for €25–30, but if positioned as a premium, drinkable beauty ritual, it could easily command 30–50% more. Consumers want experiences, not just clinical tasks. Yet Western VMS manufacturers stick to dry formats because liquid production is more challenging, technically complex, and harder to stabilize. As a result, they transfer the problem to consumers, who then make compromises.

The future won’t accept that compromise. Functional shots, ready-to-drink beauty elixirs, and daily blends are expected to surpass powders and pills in the next decade. As shelf fatigue meets pill fatigue, “beauty you can sip” is set for rapid growth. What’s missing? Scaled liquid production, improved taste science, and brand stories that match label promises with daily routines.

Consider collagen. The global market is valued at $10–19 billion [2], with a large portion directly tied to beauty claims such as skin elasticity, anti-aging, and hair strength. Add functional beauty drinks: conservative estimates suggest this segment is worth another $2–4 billion. However, a quick look at convenience store shelves in Tokyo or Seoul shows these numbers likely underestimate the reality. Walk the aisles and you’ll see collagen shots, hyaluronic boosters, and brightening elixirs—scenes that rarely appear in Western analyst reports.

Then there’s the overlap. Immunity blends, detox shots, and protein powders with a beauty twist all merge into the same concept: inner beauty. When you consider this crossover, the actual nutricosmetics market isn’t $8 billion; it’s closer to $50 billion and growing.

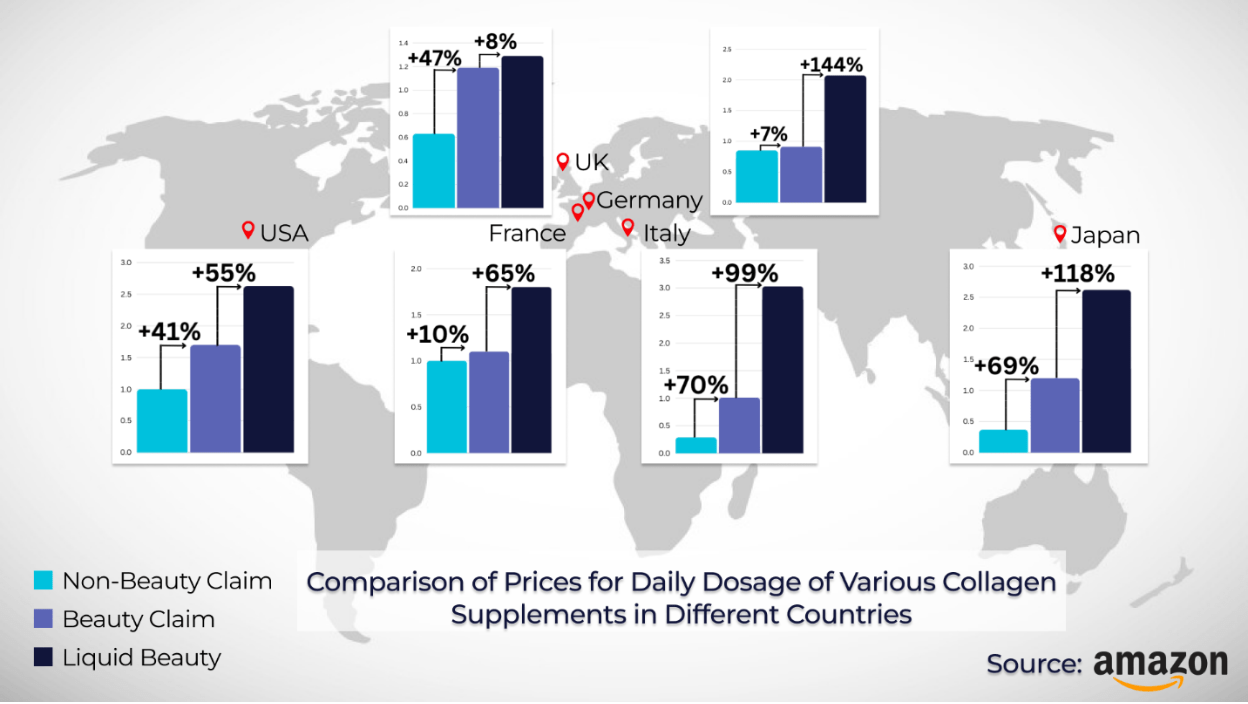

And price tells the same story. A survey of Amazon prices across Japan, Italy, and Germany shows that liquid beauty formats cost between +99% and +144% more than non-beauty claims, and +7% to +70% more than dry beauty SKUs [3]. Same active ingredients, different format, and suddenly, perceived value doubles.

Industry insiders already know this, even if they don’t say it out loud. At a recent VMS summit, the slides showed a familiar scene: flat or single-digit growth for pills, capsules, and powders. But one isolated bar, labeled “Other,” indicated +25% growth, a polite placeholder for liquids. No detailed breakdown. No analysis. Just a shrug. We understand what that “Other” represents. It’s where the action is and where legacy VMS players lack the tools, capacity, and flavor tech to compete. So it remains conveniently overlooked.

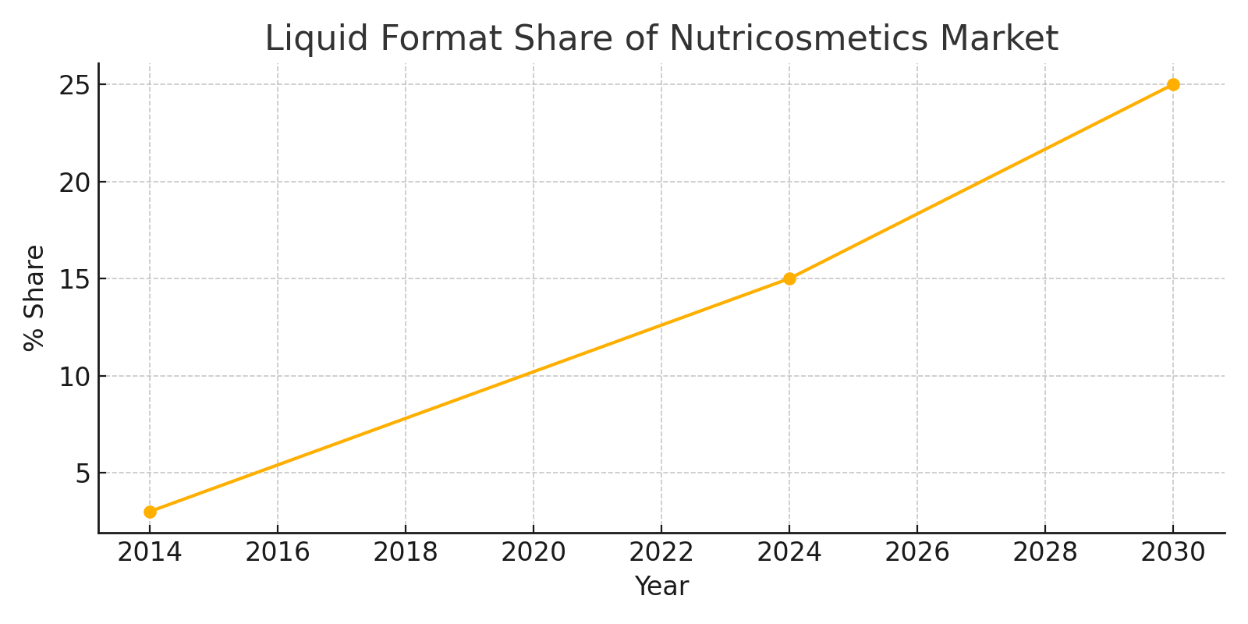

But overlooked doesn’t mean insignificant. Ten years ago, only 1–3% of VMS was bottled in liquid form. Today, that share is 13–17% and growing at 1–1.5% per year [4]. This quiet CAGR might not appear on polished analyst slides, but it’s quietly shaping future winners. Over the next five years, this so-called “Other” will be where billion-dollar brands emerge. To see it clearly, you must look inside the black box, and realize it’s not “Other” at all. It’s the future.

The True Format Breakdown: How the Hidden $50B is Structured

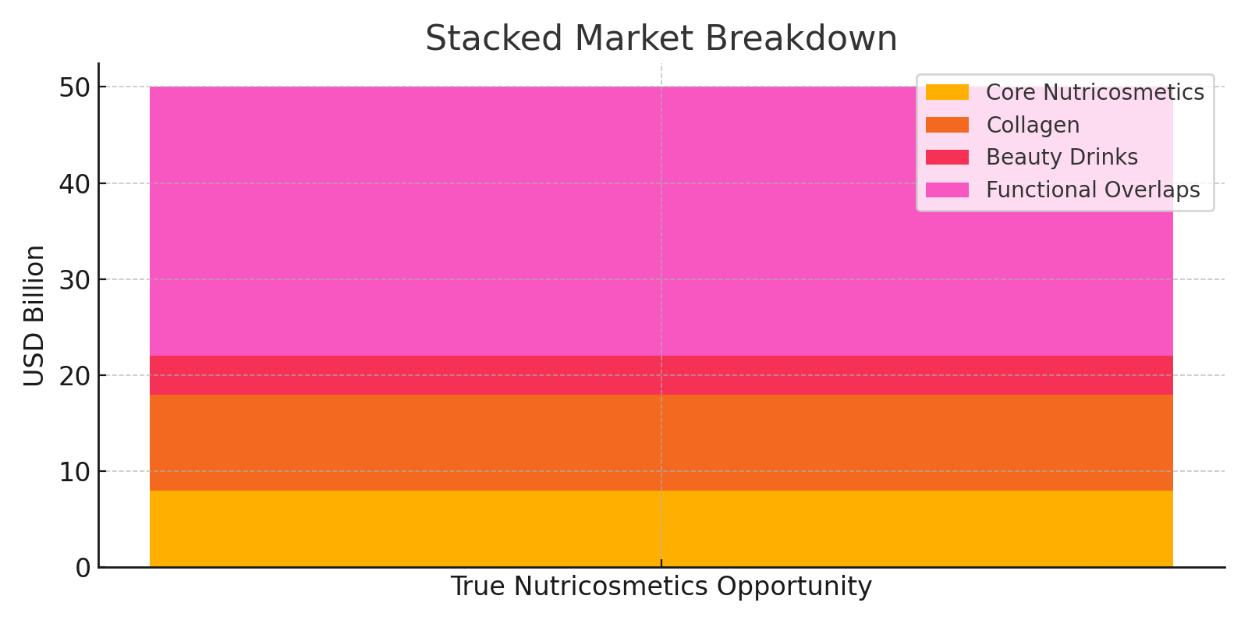

Peel back the polished category slides, and the nutricosmetics landscape reveals itself to be much larger and more chaotic than most reports suggest. The $8–10 billion figure that brands regularly cite is just the visible core: clearly labeled beauty supplements like skin collagen blends, nail and hair boosters, and elastin-rich drinks sitting on pharmacy shelves. It’s the cleanest part of the category and also the most deceptive.

Because that figure doesn’t include the deeper spending hidden behind overlapping claims. Globally, collagen alone accounts for $10–20 billion in sales, much of which is still labeled as joint health, sports recovery, or healthy aging. However, the core consumer motivation often returns to the same promise: firmer skin, smoother texture, and a more youthful appearance. When you add Asia’s functional beauty drinks with normalized staples, not novelties, you gain another $2–4 billion. Plus, if you expand further to include immunity shots, detox blends, and ready-to-drink wellness formulas that suggest beauty benefits, the total rises to $15–20 billion more.

Then come the subtle borders: gut health powders marketed for digestion but quietly targeting the skin-gut axis, melatonin blends that slip in anti-aging claims, protein drinks that sneak in collagen and elasticity messaging. These related wellness products, hard to classify but easy to recognize, represent another $15–20 billion in crossover spending. Combine it all, and the true figure emerges: nutricosmetics, a $50 billion market woven through wellness, food-tech, and functional nutrition, just hidden in plain sight.

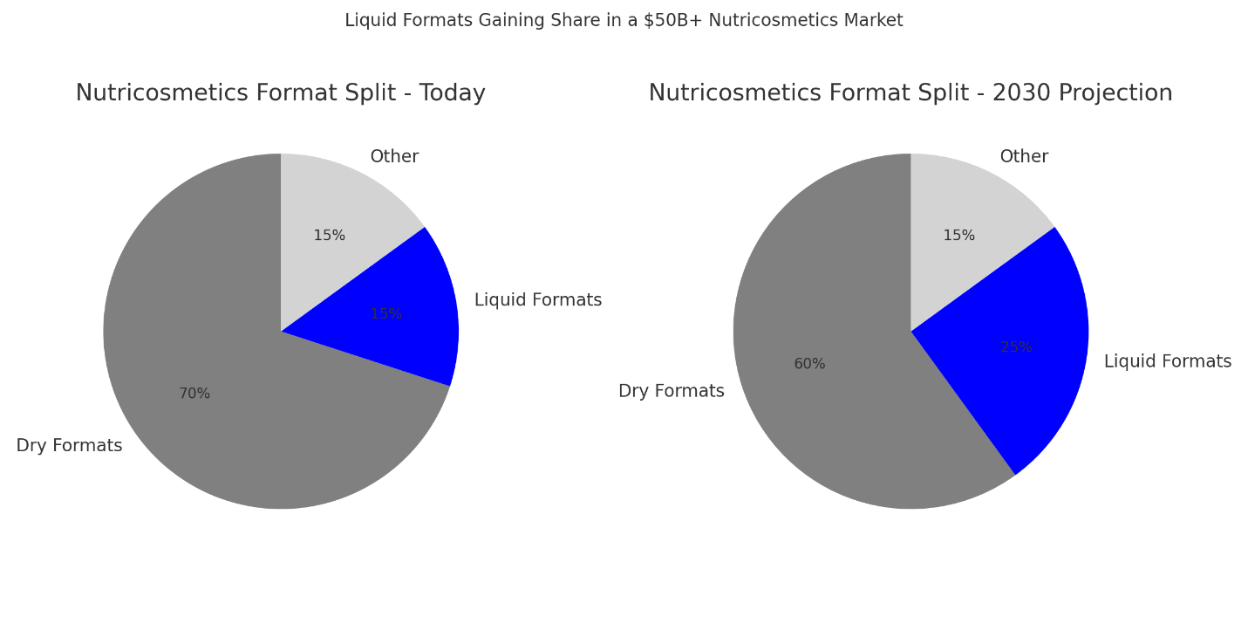

The key factor is how the product is delivered. Currently, about 70% of category spending goes to dry formats: tablets, capsules, powders, and gummies. These traditional formats are inexpensive to produce, simple to ship, and based on decades-old manufacturing lines designed for vitamins and sports nutrition. Liquid ready-to-drink formats like shots, ampoules, and elixirs make up only 15% of the market. They are usually listed as “Other” on charts, acting as a placeholder for what most factories still can’t produce at scale. The remaining 15% is divided between hybrids such as chews, sticks, and functional foods. These are products that technically push innovation, but economically act like dry SKUs: thin margins, rarely repurchased, and easy to discontinue after one cycle.

However, only one segment is gaining ground. Liquids, which made up only 1–3% of the VMS market a decade ago, now account for 13–17%, increasing by about 1 to 1.5% annually. If current trends continue, the market will rebalance by 2030: dry formats will decrease to around 60%, liquids will grow to 25%, and hybrids will stay steady. Even if the overall category remains flat, that shift alone makes liquid nutricosmetics worth $12–13 billion. If the category expands to $60–70 billion, which is likely due to premiumization and wellness trends, liquid formats could hold $15–17 billion of that total.

This shift extends beyond numbers and signals an economic change. Similarly, value is now defined more by the format than by volume. A €20 powder jar might sit unused in the cupboard, while a €40–60 ready-to-drink beauty bottle is finished to the last drop and repurchased every month. Even if liquids make up only a quarter of category units, their revenue can exceed 30–35% of total value. That’s not just a forecast; it’s the new core.

At the heart of that core, along with innovation, is ritual. And it’s ritual, not ingredients or packaging, that turns a product into a way to keep customers.

Format = Ritual = Retention

In beauty, it’s the ritual that creates lasting power. The gentle repetition of a product woven into daily life, not the hype around its launch or the shine of its packaging. Ritual is what turns a promising idea into steady revenue. Month after month. Bottle after bottle.

And ritual doesn’t come from just any format. It needs to be smooth. Powders might seem efficient on paper, but in real life, they get pushed to the back of the cupboard when the routine gets boring. Pills and capsules rely on convenience, but they fade into the background of a busy day — out of sight, out of mind. Gummies? A sweet break, but sugar hardly builds loyalty.

Liquids behave differently. They don’t just disappear. They stay on the counter, in the fridge, next to the toothbrush or the morning coffee. They become part of the routines people already have. And taste, often dismissed as cosmetic, becomes the foundation. Get the flavor right, and the habit follows. Habit turns into ritual. And unlike novelty, ritual lasts.

The data strengthens the case. Among millions of units produced, liquid nutricosmetics have an average monthly retention rate of 60%, with users coming back twelve times a year. Dry formats, on the other hand, are often only repurchased quarterly, if at all. The economic impact is clear: a €30 liquid bottle, used and rebought each month, provides €360 in yearly value. A €30 pill pack, restocked once per season, totals only €120. Same active ingredients. Different format. Significantly different return.

Why is there a gap? Flavor. Taste encodes memory. A product that tastes good becomes something remembered and even craved. That’s why so much investment has gone into flavor masking, precision blending, and microbiological stability. A successful liquid has to be a diluted supplement, with a carefully engineered system: one that balances science, palatability, preservation, and consumer experience.

And the next generation? They’ve already expressed their preferences. Recent global data shows that 41% of Gen Z consumers choose liquids or ready-to-drink wellness products along with traditional options like powders and pills. Baby Boomers, in contrast, stay more loyal to tablets [5]. In other words, the future is already leaning toward fluid formats that suit flexible lifestyles.

That’s the true moat. A format that aligns with how people want to feel beautiful every day. When that ritual becomes consistent, brands no longer need to rely on discount codes or gimmicky loyalty programs. They simply have to keep offering something good enough to bring people back. Because in beauty, as in wellness, retention is built, not bought. And the driving force behind it is liquid.

Format as the Profit Engine: How Daily Liquids Redefine Value

When discussing the future of beauty-from-within, it’s not enough to focus solely on what’s being sold. How it’s delivered is just as important. The supplement aisle still clings to the illusion that all formats are interchangeable, as if a powder scoop, a pill bottle, a gummy jar, and a liquid shot provide the same value, just in different forms. However, the market paints a different picture. Format acts as a lever that influences behavior, determines how products are used, and ultimately decides who will return.

Line up four formats side by side: pills, powders, gummies, and a 500ml liquid bottle, and the differences start to add up. The ingredients may be the same, the claims identical. But what happens after they leave the shelf is what really matters.

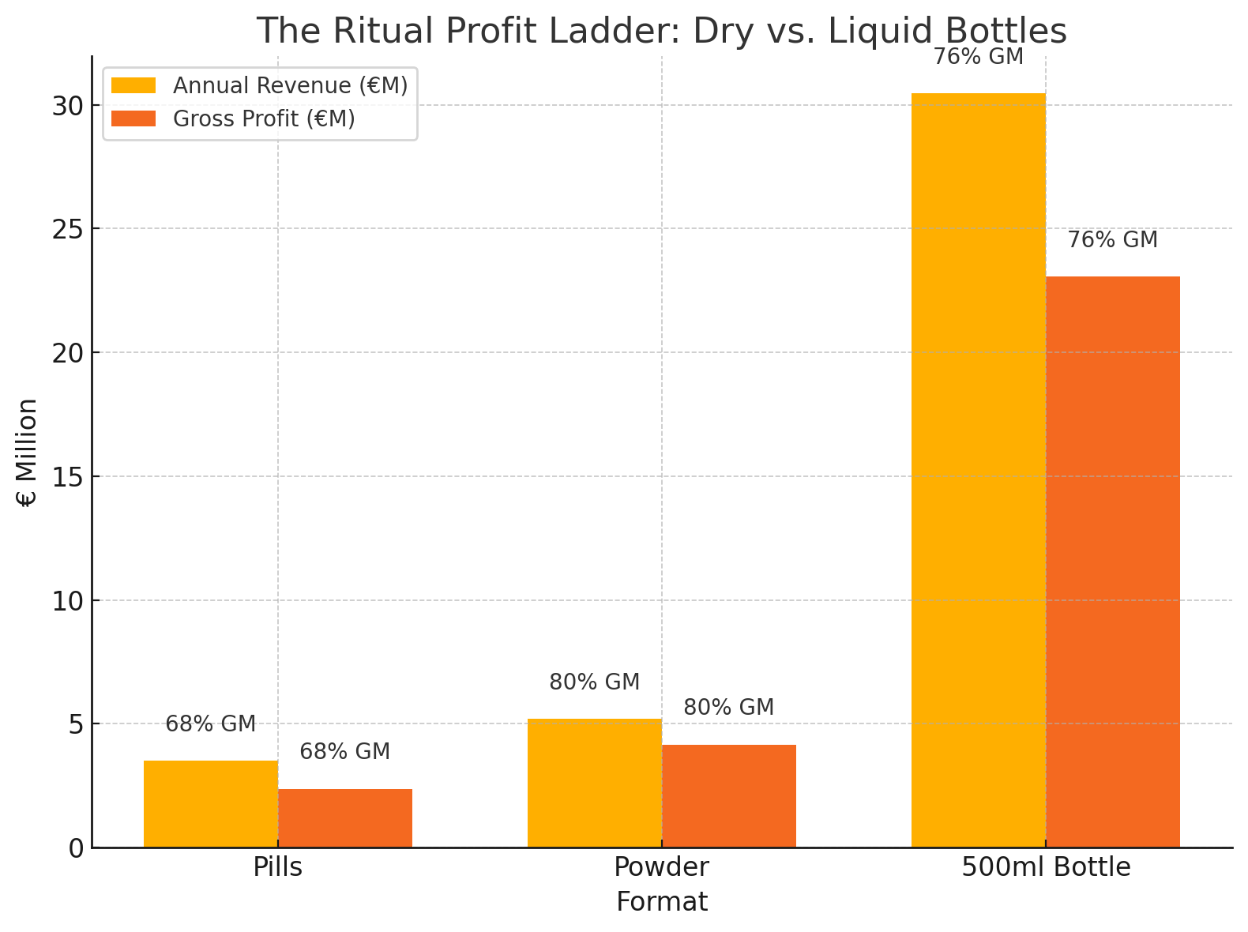

Assume each brand launches with 100,000 units. Pills, a 30-day supply, typically sell for $25. Production costs are low (about $8 per bottle). Powders last longer: a 60-day supply might sell for $40, with similar costs per unit. However, compliance drops. Powders are often half-used, and pills are forgotten. Reorder rates stay between 30 and 40 percent within three months.

Now compare that to a 500ml liquid collagen product designed for daily use. It sells for $35–$55, with production costs around $8.50 due to added flavor work, preservation challenges, and premium packaging. But here, the outcome changes. The product is consumed. The habit sticks. The bottle empties and triggers a repurchase. Retention jumps to around 70 percent monthly, which is more than double the rate of dry formats.

Math speaks for itself. A pill brand might generate €3.5 million across 140,000 units, maintaining a 68 percent gross margin. Powders can edge that out slightly, bringing in €5.2 million at an 80 percent margin. But the liquid format, with a slightly lower unit price and higher repeat rate, generates €30–31 million annually, maintaining a 76 percent margin. Fewer units. Far more value.

This is where the economics of ritual come into play. That €8 powder tub might be sold once and then forgotten behind the olive oil. A €35 liquid bottle costs a little more to produce, but it’s used completely and purchased again every four weeks. Even if liquids make up just a sixth of the category’s volume, they typically contribute over 30 percent of the revenue, and in mature markets, closer to 40 or 50 percent, especially as beauty drinks become mainstream behavior.

This isn’t just theory. It’s evident in Japan, where Shiseido’s beauty beverages consistently outperform powder sachets year after year. It’s also seen in Fancl’s collagen ampoules, which have kept their premium prices while gaining market share. That’s why forecasts from Grand View Research, Euromonitor, and FMCG Gurus still project liquid formats to lead the growth trend.

Modern consumers, especially Millennials and Gen Z, seek functional ingredients in formats that easily fit into their lives. They prefer a routine they can follow without needing to remember it. That’s why liquids are popular.

The main point is simple. Format isn’t about volume. A daily liquid habit commands a premium, and the ritual helps ensure repeat purchases. A powder jar might sell once for €40 and then be forgotten. A 500ml bottle, priced similarly, gets finished, repurchased, and repeated twelve times a year. It may hold less by weight but offers more by value. That’s not a prediction. It’s already happening. And to see it clearly, just look East.

Asia Shows the Future

If you want to see what happens when inner beauty overcomes outdated standards, look East. In Japan, China, and South Korea, the idea that beauty begins inside the body is already a part of everyday life.

Walk into a convenience store in Tokyo, and the shelves speak for themselves: rows of sleek bottles offering collagen blends, hyaluronic acid shots, and antioxidant-rich tonics. Shiseido didn’t build its longevity on topical serums alone. Its beauty beverages have held premium shelf space for more than two decades, positioned alongside Fancl’s collagen drinks and AmorePacific’s functional elixirs. In this market, the beauty ritual doesn’t end at the bathroom mirror. It continues into lunch breaks, gym bags, and evening routines that seamlessly fit into modern life.

Asia’s shelves reflect how supply evolves with demand. The infrastructure wasn’t just adapted for liquids; it was built specifically for them. There was no debate over feasibility. These formats weren’t questioned; they were anticipated. Consumers led the way, and the category followed. Real ingredients, real results, delivered in a taste-focused experience that was easier to use.

This is why Asia now accounts for an estimated 45% of global nutricosmetics spending, much of which is through liquid formats [6]. In Japan, beauty drinks occupy prime retail space, consistently priced higher than their dry-format counterparts. In China, the growth has been even more rapid: from a niche category to a $3.7 billion edible beauty segment in less than a decade, driven by the cultural normalization of daily shots and functional beverages [7].

This environment operates without a gatekeeper. No regulatory bottleneck or plant manager blocks innovation by claiming liquids are “too difficult” or shelf life is too risky. Instead, consumers lead the format evolution, and brands that listen are adapting. The same consumer, when given a choice, doesn’t pick the jar hidden behind the olive oil. They choose what stays in the fridge or travels easily in a bag. And they do it again tomorrow.

Asia’s leaders didn’t stumble into this position. They invested early in infrastructure, taste systems, and shelf logic built around habits. That repeat loyalty didn’t require a discount strategy. It needed format alignment.

So why hasn’t the West caught up? The main barrier is production. The factories that thrived during the powder-and-pill era can’t easily be adapted for high-volume liquid manufacturing. Most haven’t even tried. Instead, they stick with old tools: capsules, sachets, and shelf-stable jars, while the East moves forward, bottle by bottle, sip by sip.

Overlay that retail reality onto spending patterns, and the regional hierarchy becomes clear: Asia leads, the U.S. is gaining ground, and Europe is currently remaining steady.

Where It Lives: Asia Leads, USA Catches Up, Europe Holds

Follow the actual spending by format, and the picture becomes clearer. The so-called $50 billion nutricosmetics opportunity is already developing. The only question is where it’s speeding up next.

Asia-Pacific still dominates. The region accounts for about 45% of global beauty-from-within spending, which we estimate at $22–23 billion today. Here, shelf alignment is strongest: Shiseido’s RTD beauty drinks are placed beside Fancl’s ampoules, while convenience stores in Japan and Korea display collagen shots along their aisles. Consumers expect liquids as a standard part of their routines. When we examined Shiseido’s growth, Asia’s share of the global category was close to 50%, and that same figure remains when focusing on dedicated nutricosmetics.

But the West is catching up quickly. In North America, mainly driven by the United States, nutricosmetics now account for 30–35% of global spending, up from just 15–20% a decade ago. This growth is driven by a mix of trends: collagen peptides expanding beyond sports nutrition, the mainstream acceptance of wellness shots, and a cultural shift that views supplementation as a lifestyle choice rather than an obligation. American consumers are ready, both in desire and spending power, to go further. However, they are limited by outdated supply chains. Liquids remain an open opportunity: validated in Asia, popular among younger consumers, yet still largely missing from store shelves. Due to a manufacturing gap, few legacy VMS plants are willing or able to address this issue.

Europe and the UK, by comparison, stay steady at 20–25% of global spend, worth $10–12 billion today. This region laid the clinical groundwork for collagen long before U.S. consumers took notice. European buyers trust the science. However, the market has not yet shifted to ritual formats. Powders, sachets, and tablets still lead. The belief is there. The behavior is not yet. Like in the U.S., shelf inertia is the main obstacle, not consumer resistance.

The pattern is clear. The earlier outlined format shift—from 15% of the category in liquid formats to over 25% by 2030—directly aligns with revenue potential. Asia demonstrates what happens when infrastructure centers on consumption. The U.S. shows the benefits once manufacturing expands to meet demand. Europe proves consumer confidence, waiting for product experiences to meet their expectations.

But for that shift to happen, something has to give. The current production model is designed for dry goods and optimized for smooth logistics, but it won’t bring the next chapter. If existing factories can’t adapt, new ones will have to take the lead. Because the shelf won’t wait forever. And consumers, more and more, already know what they’re missing.

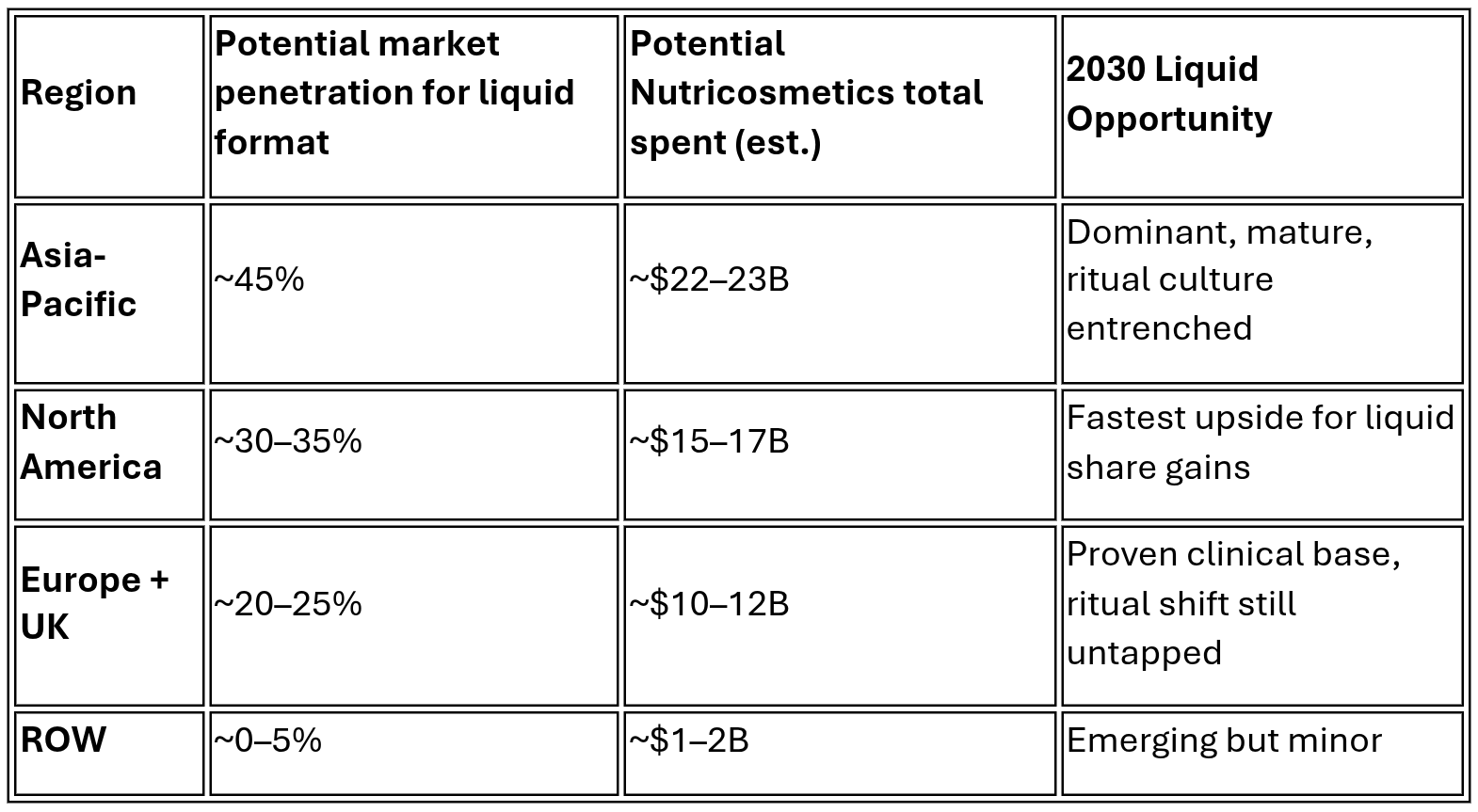

This table shows TOSLA’s 2030 projections for liquid nutricosmetics penetration by region, based on internal modeling. Asia-Pacific leads with approximately 45% share and established consumer rituals, while North America exhibits the fastest growth potential, with up to $17 billion in spending shifting toward liquid formats. Europe’s science-driven market is prepared but underutilized, and the rest of the world remains marginal for now.

The Industrial Bottleneck

So why, with the evidence stacked across Asia’s shelves and demand rising in every market survey, does the West stay tied to dry formats that consumers ditch before spring? The answer lies in the industry, its capacity, and who controls it.

The vitamin, mineral, and supplement (VMS) sector didn’t stick to powders and pills just out of tradition. It developed around them for a reason. Dry formats are inexpensive to produce, simple to store, and lightweight to ship. They don’t require flavor systems or advanced preservation. Their shelf life is measured in years. And they fit smoothly into legacy infrastructure, the same production lines that have been making tablets for decades. When your factory floor is optimized for compression, not mixing, innovation becomes secondary to operational efficiency.

Liquid changes the game. You can’t just dissolve an active ingredient in water and call it a day. Developing a effective and good-tasting beauty drink means solving a series of problems that most factories were never designed to handle. Hero ingredients often taste bad or oxidize when exposed to air. Potent mixtures can clog lines, foam during filling, and need specialized valves to prevent cross-contamination. Flavor masking must be precise, and microbiological safety must be absolutely reliable. If the product is meant to stay in someone’s fridge rather than their supplement drawer, then its shelf life should be measured in months, not days. None of this fits inside a line built for gelatin capsules and sachet fillers.

And so, the industrial response is predictable: nudge brands back toward the familiar. “Start with a capsule,” they say. “Maybe try a powder. A gummy if you want to be edgy.” But what they’re really saying is: don’t challenge our machinery. The result? SKUs that hit the market with little intention of lasting. Products that gather dust in cabinets. Promotions built on discounts instead of experience. And a customer journey that ends in March.

Stubbornness isn’t the real issue. It’s about systems. A CapEx decision is only a small part of the process, since retooling for liquid demands a complete rethinking of the entire supply chain. It requires clean rooms, aseptic fillers, preservative models, live NPD, regulatory adjustments, and a sensory science layer most VMS firms have never had to learn. It’s no wonder they don’t make the leap.

But that’s exactly where the opportunity exists. Consumers are prepared. The shelf is stocked. The infrastructure, however, isn’t. That’s the gap—and it’s the same gap TOSLA was created to close. We focused on flexibility: custom compounding, live formulation labs, and a flavor science stack that even turns the toughest actives into daily habits. Liquid isn’t just an extension for us; it’s our operating system.

The irony? The same analysts who categorize liquids as “Other” on their slides are now seeing that “Other” chip away at core market share. From just 1–3% of VMS formats a decade ago to 13–17% today, liquids are steadily gaining about 1–1.5% market share annually. However, that growth remains theoretical for most, unless you can actually produce the product.

The brands that will succeed in the next five years aren’t just following trends. They’re ignoring traditional hierarchy and partnering with those who can turn a real ritual into a product. This isn’t about chasing hype. The secret is owning the daily sip and building a system that allows for scale.

The Liquid Imperative

Beauty is an industry that prides itself on identifying the next big trend before it hits the balance sheet. Yet, the signs couldn’t be clearer: evidence piled up on shelves from Tokyo to Seoul, a new generation seeking beauty in a daily sip, and they already accept a premium price. Still, too many Western brands are stuck promoting formats designed for legacy factories, not real-life situations.

The message is clear: format can no longer be seen as just a secondary aspect of product development. It has become a vital and defining part of the product itself. The same collagen peptides, antioxidants, and hyaluronic acid produce a completely different result when contained in a ritual-ready liquid versus a clumpy powder or an invisible pill. When done correctly, the format can deliver results and simultaneously foster retention without gimmicks, loyalty without burnout, and margins that last beyond the next influencer trend.

Asian markets spotted this trend long ago. Shiseido’s ongoing leadership in the drinkable beauty market didn’t happen by accident; it resulted from deliberate strategic choices, matching product formats with consumer habits and seamlessly incorporating technology into daily routines. The outcome? Products that fit in handbags, fridges, gym bags. Products that are used until finished and bought again. Now, as Western brands try to catch up, they’re still relying on machinery that was never designed for this.

A capsule doesn’t create a ritual. A gritty powder that separates in water doesn’t feel premium. This is where the edge is now—in the infrastructure that transforms sensory experience into daily habits. The brands that succeed won’t be the ones clinging to traditional supply chains. They’ll be the ones partnering with specialists who have made liquids scalable, stable, and delicious.

Because when a ritual succeeds, the shelf stops being a gamble. It turns into a fortress for the select brands brave enough to capture it perfectly.

The numbers reveal the full story. Liquids have quietly increased from 1–3% of VMS volume a decade ago to 13–17% today, growing at 1–1.5% annually. What was once called “Other” is now the most significant segment, and it won’t be captured by plants built for tablets.

The numbers don’t lie. What was once a hidden 1–3% of VMS volume is now 13–17%, adding another 1–1.5% share every year. The “Other” that polite market slides dismiss is now the only slice worth fighting for, and it won’t be won by factories telling brands to settle for capsules.

That’s why TOSLA exists. Not to chase the old SKU logic, but to create a system centered around liquid beauty rituals: flexible formulations, clinical flavor systems, and format science that transforms hero ingredients into habits worth repeating. And the demand is already underway.

Our research indicates that by 2030, North American consumers alone will increase their yearly purchases of beauty liquid supplements from approximately 40–50 million units today to 120–150 million. Europe will follow with an additional 70–85 million bottles. Combined, that’s over 200 million bottles annually, each designed to support a 12x repeat cycle instead of a quarterly one.

With an average retail price of $35 per bottle, North America will generate $4.7 billion in revenue; Europe, $2.7 billion. After retail and distribution costs, that amounts to $3.7 billion in ex-factory turnover. And with liquid margins of 70% or more, it results in over $2.6 billion in gross profit.

This is no longer just the realm of powdered supplements or traditional multivitamins. It also won’t be fragmented among countless small-scale producers. The complexity of liquids, including flavor systems, preservation challenges, and the need for high-potency and active stability, naturally creates a bottleneck. The likely result? An oligopoly—similar to a Red Bull-style model for beauty and wellness—where five to eight vertically integrated ecosystems control the format, the ritual, and the entire value chain.

Red Bull transformed a functional drink into a ritual repeated billions of times annually, commanding a price well above its raw input costs. Nutricosmetic liquids are following the same trend, with five to eight players generating volumes and margins comparable to regional Red Bull units. These brands generate over one billion euros in yearly net revenue and more than €600 million in gross profit. While not on the same scale as cola, they are enough to reshape how supplements view loyalty, habit, and format as strategic tools.

Each of those bottles must be formulated, masked, blended, filled, and prepared for shelf. That production line doesn’t exist in the old pill plants. It’s operated by specialists who understand taste, know how to stabilize bioactives, and design for ritual.

For brands, this opens a new profit margin structure and increases lifetime value. For suppliers ready to seize the opportunity, it reveals an entire €3–4 billion market that has been hidden under the label of “Other.”

The next billion-dollar shelf won’t come from hype but from bottlers who transform a daily sip into millions of consistent, profitable rituals.

At TOSLA, we are leading the charge into the liquid format era with science, flexibility, and sensory power, essential for transforming a great active ingredient into a great habit. The market is shifting. Investment patterns are changing. The infrastructure must adapt or fall behind.

Sources & Footnotes

-

Straits Research, Nutricosmetics Market Size, Share, Trends, Growth 2024–2033: https://straitsresearch.com/report/nutricosmetics-market

-

Grand View Research, Collagen Market Size Report, 2024–2030: https://www.grandviewresearch.com/industry-analysis/collagen-market

-

Tosla Internal Analysis, Amazon Pricing Scan (2024)

-

Tosla Internal Tracking, Liquid Format CAGR and Share, 2014–2024

-

NBJ / Vitafoods Insights 2024 Consumer Format Survey

-

Precedence Research, Asia-Pacific Nutricosmetics Forecast: https://www.precedenceresearch.com/nutricosmetics-market

-

Vogue Business, China’s Edible Beauty Boom: https://www.voguebusiness.com/beauty/just-how-yummy-is-chinas-edible-beauty-boom